Schedule III Cannabis Insurance: Why Rescheduling Renders Your D&O Strategy Obsolete

As the cannabis industry shifts toward Schedule III, the legal and financial stakes have never been higher. This guide explores how the end of 280E tax burdens will spark a wave of M&A activity and new litigation risks. You will learn why legacy insurance policies are now obsolete, the critical importance of “Institutional Grade” D&O coverage for securing funding, and how specialized protections like Side A DIC and R&W insurance safeguard your personal assets during an exit or expansion.

Have you heard the news? The DEA is considering moving cannabis to a Schedule III substance. This change in federal law would fundamentally shift the cannabis industry, immediately getting rid of the 280E tax burden that has crippled companies and shifting the legal foundation upon which cannabis businesses are built.

Rescheduling does more than provide a tax windfall; it creates urgent insurance needs to keep your company properly covered. Policies like D&O insurance written for a federally illegal substance are completely mismatched with the coverage needed for a federally regulated one. And with changes in cash flow and insurance comes a new risk for MSO and enterprise-level leaders; scrutiny that comes with the flood of institutional capital.

The 280E Dividend and the New Litigation Landscape for Cannabis Businesses

The elimination of 230E is a huge relief for cannabis companies, and many MSOs are already eyeing a pivot towards M&A and R&D with 280E tax dividends. The possibility of having “new cash” on hand and being able to take ordinary business expenses deductions is thrilling in an industry that has long been cash-strapped.

But this change in liquidity for cannabis companies also makes them more attractive targets for Securities Class Actions and Derivative Suits filed by shareholders. This deeper pockets conundrum will play out as fewer “disclosure of regulatory raids” and more “breach of fiduciary duty” as cannabis MSOs experience a large change in liquidity.

Why Your Current D&O Policy Is Obsolete

Many existing D&O policies have language written for a Schedule I substance and may contain specific exclusions for substances in the Controlled Substances Act. This creates legal grey areas for cannabis companies during the transition to Schedule III within the scope of cannabis insurance.

If your D&O policies contain this language, it needs to be spotted and changed immediately. Leaders need to negotiate “Broad Form” D&O wording with insurance carriers in order to take full advantage of the growth that Schedule III and legalizing cannabis federally brings.

Traditional high-capacity carriers and financial institutions have stayed away from cannabis because of the risks associated with insuring a substance with federal restrictions. But movement to Schedule III, with accepted medical use and the possibility of interstate commerce, is the green light for them to enter the market. It also opens the door for companies to shift from expensive “surplus lines” for insurance to the more competitive, traditional “admitted” insurance market.

How to Insure Your Exit or Expansion in the Cannabis Industry

As the cannabis industry braces for a historic shift following federal rescheduling, securing the right insurance architecture is no longer just a defensive move—it is a prerequisite for a successful exit or expansion.

The M&A Surge: Insuring the Transition of Power

Changing federal law to make cannabis a Schedule III substance will trigger a “valuation correction” across the industry. This will likely lead to a wave of consolidation as smaller to mid-size MSOs seek to exit the industry due to the burden of complying with FDA regulations, and large MSOs seek to fill the map with acquisitions.

Transition of leadership in an acquired company is a delicate and risky time, but the proper umbrella of insurance coverage can help the process move more smoothly. R&W insurance (Representations and Warranties) is an M&A-specific policy that protects the buyer from “unknown” liabilities (such as tax gaps or undisclosed litigation) while allowing the seller to walk away with more cash at closing

Past issues can creep up, and present issues for sellers and buyers, but cannabis insurance can mitigate risk. A R&W policy is vital for buyers to ensure they won’t inherit any legacy tax issues around 280E. D&O insurance with a “tail” or run-off coverage keeps personal assets of previous leadership protected from lawsuits once the company is sold. Without a “tail” policy, previous leaders could be on the hook for decisions made years ago.

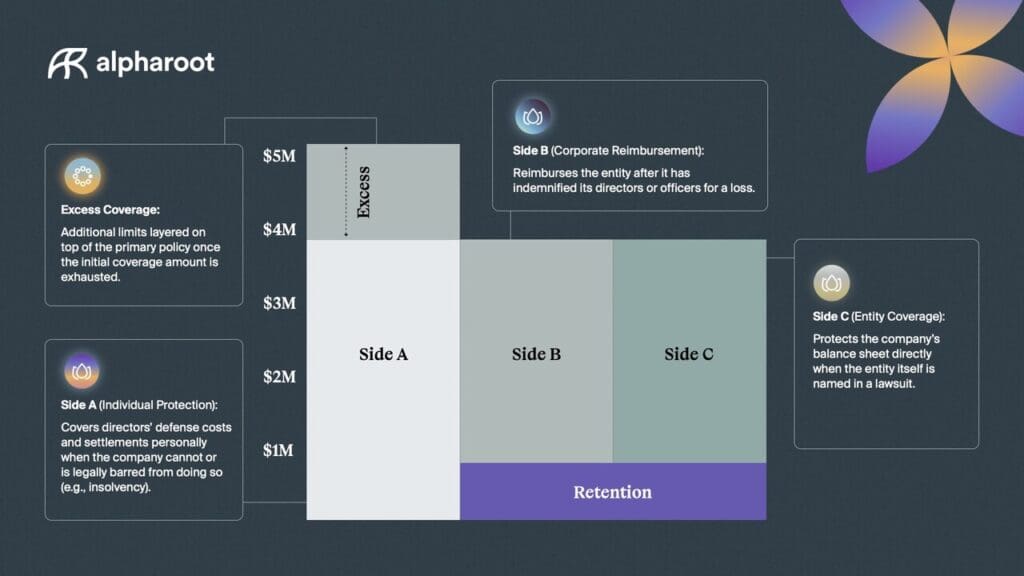

The Enterprise Tower: Understanding A, B, and C Coverage

Directors and Officers policies offer protection from lawsuits in three layers: Side A, Side B, and Side C.

Side A: Individual Protection

This layer personally protects named directors and C-suite executives. It kicks in during a lawsuit when the company cannot pay or is not allowed to pay an individual, either due to financial problems (insolvency) or legal reasons (derivative suits). Sometimes called a “personal safety net” for personal assets.

Side B: Corporate Reimbursement

This is typically the most active layer of a D&O policy. When a company indemnifies individuals named in lawsuits and pays for their defense, Side B pays the company back for those costs. However, the individual must already be named in the D&O policy.

Side C: Entity Coverage

If a corporation is named in a securities or regulatory lawsuit, Side C protects the balance sheet, reimbursing costs and settlements. (Note: For public companies, Side C is typically strictly limited to “securities claims.)

The “Extra Shield”: Dedicated Side A DIC (Difference In Conditions)

D&O policies exist to protect a company during its most vulnerable time, during a lawsuit. But in major suits against MSOs, Side C, Entity Coverage, can often “eat up” the policy limits, taking payouts to the ceiling of the policy. This leaves Side A, Individual Coverage, exposed. Since D&O coverage was originally created to protect individuals, it creates an intolerable gap for experienced board members.

The answer lies in an additional piece of coverage in Side A D&O: a dedicated Difference-in-Conditions (DIC) policy. This excess coverage sits outside the main D&O policy. It ensures that even if the main policy is exhausted through other means or the company goes bankrupt, individual directors still have a dedicated pool of defense funds.

The Investor Mandate: Why Quality D&O is a Funding Requirement

Your insurance coverage matters more than you think in a post 280E-world. Institutional investors require a lot from the companies they work with. Most Tier 1 Lenders, private equity firms, and family offices view D&O insurance as a proxy for corporate governance. No lead investor will take a board seat on an MSO that does not have protections for company leaders, including “Institutional Grade” D&O.

Additionally, a clean D&O profile is a green flag to the investor market that an MSO is “Exit-Ready” or “IPO-Ready,” with the capacity and organization for a clean transition. This can lead to more favorable terms for expansion funding rounds and even research and development.

In short, for companies of a certain size, D&O insurance is either a major opportunity or a business ceiling. Download our D&O Readiness Checklist to determine where you stand.