The Hidden Multiplier: How Budtender Salary Hikes Impact Your Workers’ Comp Premium

Think a $3 raise only costs $3? In the cannabis industry, “hidden” multipliers like Workers’ Comp premiums and payroll taxes can nearly double the actual cost of a wage hike. This article breaks down the Salary Sensitivity Analysis every owner needs to avoid year-end audit traps. Discover how increasing pay can actually lower your long-term insurance rates by slashing turnover and improving your EMOD “golf score.” Master your total human capital costs today.

The cannabis industry has been built on the backs of hard-working people in the legacy and legal markets. In the legal cannabis market, many entry positions are minimum wage, but in the last year, there has been a large push to increase the standard hourly pay of many workers, particularly budtenders. In some competitive markets, pay has jumped as much as $6 – $8 an hour, going from $15 or $16 an hour to $22+.

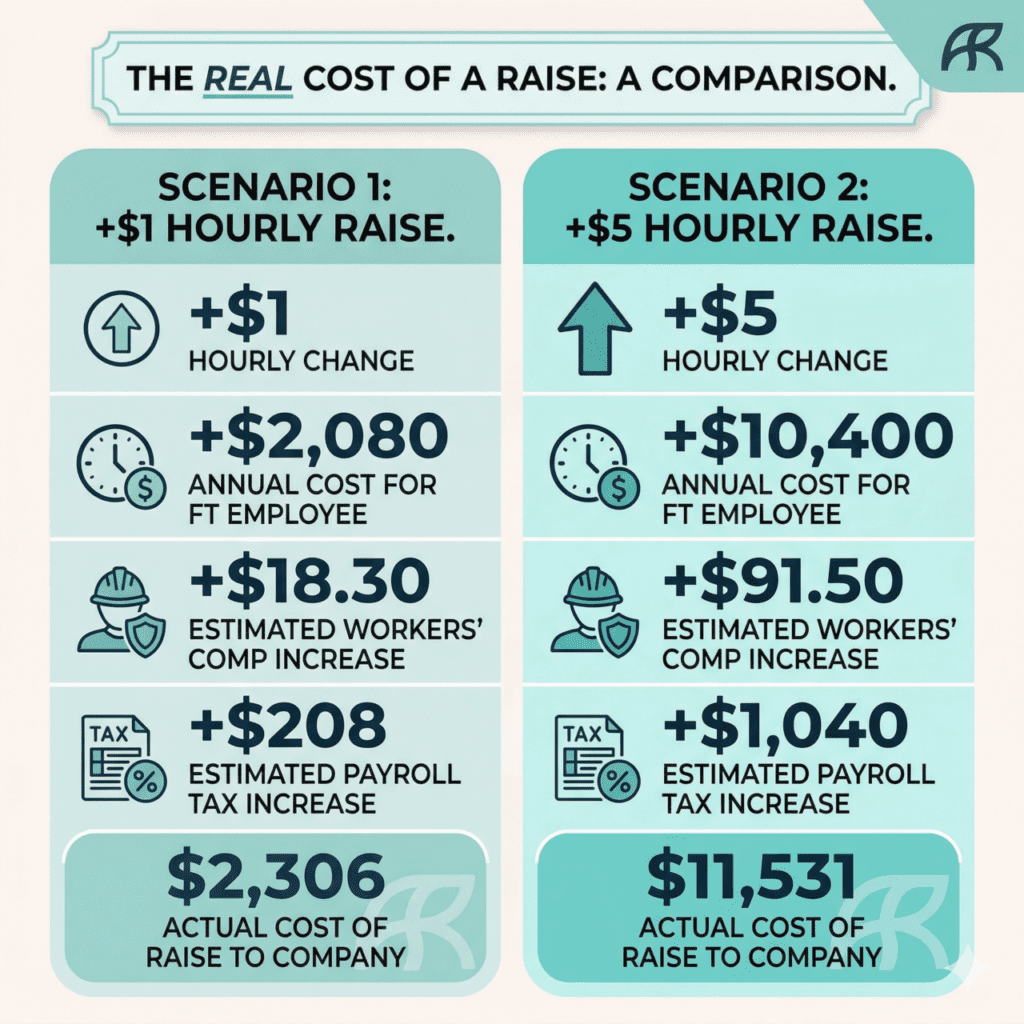

Many business owners calculate the cost of a raise by looking at the hourly difference. But a change in payroll expenditure is not the only place a wage increase changes the math. In risk management, it can also change your exposure. Payroll expenses and workers’ comp costs go hand in hand, and raising wages may also increase your insurance premiums.

The Math of the Multiplier

When calculating the cost of a pay increase, look beyond the initial change in your payroll expense to factor in changes to your insurance premiums, as well.

How are Workers’ Comp Premiums Calculated?

Every time your payroll changes due to a raise, your workers’ compensation costs change by the same amount. If you give a 20% raise, your premium may go up 20% as well.

The formula to calculate Workers’ Comp premiums is:

(Payroll rate ÷ 100) x Class Code Rate x Experience Modifier (EMOD) = Estimated Premium Cost

Note: Code 8045 is often used for drugstores or retail, including cannabis, and the rate is $0.81.

It’s important to factor this formula into your wage calculations. Many business owners only look at the exact cost, and not the total burdened cost a company is paying when workers’ comp, FICA, and FUTA are factored in. A $3 raise that brings an employee’s hourly rate to $22 actually costs the company $28/ hour, due to these additional costs.

Class Code 8045: The Retail Risk Profile

Workers’ Comp insurance rates are largely determined by NCCI Classification Codes, which determine an employee’s exposure to risk. Budtenders typically fall under Code 8045, a retail drugstore, which is not a high-risk position. But many insurance carriers are still wary of working with cannabis companies, and may add a “cannabis premium”, due to the security risk of a cash-heavy business and the ergonomic risk of repetitive motions.

Additionally, workers’ comp is one of the most heavily scrutinized insurance policies. Not only is it mandated in 49 states, it’s also audited annually. Since payroll affects workers’ comp rates, these policies must be adjusted every time pay changes. If you give your employees a mid-year raise without updating the policy, you’re liable to be hit with a large “audit bill” at the end of the year—and no one wants that.

The High-Road Hedge: Can Higher Pay Lower Rates?

Let’s be clear—budtenders deserve a livable wage. While at first glance, the math around giving raises may appear contradictory, it’s only one piece of the puzzle.

Base premium pay is tied to payroll, but Experience Modification Rate (EMOD) is tied to behavior—and that has a cost too. EMOD (sometimes called EMR) is often compared to a business credit score, where businesses are rated based on safety records. But unlike traditional credit scores, EMOD scores work like golf—the higher the rating, the worse it is. So how does the pay rate tie into this?

The “Turnover-Injury” Correlation

Statistically speaking, nearly 50% of workplace injuries occur during an employee’s first year, and go down from there. In the cannabis industry, where dispensaries face a turnover rate as high as 50%, this puts businesses in a “high-risk” zone that can increase your EMR rating and your workers’ comp premium.

One of the reasons for massive turnover is pay. Low-wage employees have no skin in the game and may bounce around in search of higher hourly rates.

In the insurance world, we call this the Gallup Gap, the gulf between the needs of a business and its employees’ levels of engagement. Low-paid workers are more likely to leave in search of better pay, and more likely to be disengaged during work, which makes them up to 64% more likely to have accidents.

Stability as a Risk Mitigator

A stable workforce helps you reduce the risk of workers’ comp claims and a high EMOD rating. The longer an employee works for one company, the more likely they are to be safe and engaged at work. It’s a kind of mental muscle memory; a veteran budtender knows the importance of a buddy lift for heavy deliveries and the idiosyncrasies of a sticky door lock—things a new employee can only learn over time. The best onboarding system in the world cannot do what experience can, and it’s valuable to retain that.

Experienced employees help reduce your EMOD score, which can offset the increase in a higher salary. High turnover in the workforce can lead to increased frequency of claims, which are small and ultimately avoidable accidents. Under the EMOD scoring system, frequent claims hurt your rating even more than severe claims do.

Consider this: a business raises its pay for budtenders, and goes from a 50% turnover rate to less than 10%. They retain their team for over 3 years, which reduces their EMOD score from 1.0, which is average, to 0.8%. This reduction in their score saves the business 20% annually in workers’ comp costs, which evens out the increased payroll cost.

Professionalism = Lower Claim Severity

People who are paid well are more likely to value and appreciate their jobs, because they’re not scrambling to make ends meet every day after they leave work. This cognitive bandwidth gives them more mental space to focus on safety protocols, compliance, and best practices.

It also gives employees a level of job satisfaction that carries over into their engagement and their willingness to follow protocol to avoid injuries and accidents. Additionally, it carries over in instances where accidents do happen, with increased willingness to post-injury protocols and “Return-to-Work” programs. This can lower the cost of an injury claim for businesses.

The “Underwriter’s Perspective”

The rates you pay your budtenders impact more than your payroll costs; it can have a ripple effect throughout your insurance policies. An underwriter who hears that a dispensary pays 20% above market rate and has 80% employee retention sees a culture of safety that goes beyond words and permeates every aspect of doing business. Having a robust security system and the best camera available is great, but if you’re replacing employees every month, there’s a massive security gap.

Consider this: a $5/hour pay hike may seem steep at first glance, but it’s significantly cheaper for a business to pay employees more in the short-term than it is to pay less and have a claim filed against the business for a new employee who got injured. Once a workers’ comp claim is filed, it affects your insurance rates for years to come.

Strategic C-Suite Moves for 2026

Raises go a long way for employee morale, but there are ways to increase pay that also increase safety awareness. Consider the following ideas as a starting point for tying pay increases to safety.

For Employees:

- Safety Incentive Programs. This program offers safety bonuses to workers, tied to your incident rates. When there are zero incidents in a quarter, everyone on the team gets a little extra money. You can even go a step further and create a “safest employee” honor for the employee who goes above and beyond for safety standards each month or each quarter.

For Business Owners and Managers:

- Invest in Safety. Many injuries for budtenders are caused by repetitive strain, or doing the same movements over and over again. Investing in safety measures like anti-fatigue mats and ergonomic POS stations can help reduce repetitive strain injuries. Posted signs around the workplace with safety reminders about buddy lifts and injury prevention can also help.

- Pay-As-You-Go Workers’ Comp: Rather than paying premiums based on quarterly or annual estimates, Pay-As-You-Go allows you to make premium payments based on actual payroll numbers. Doing so helps you reduce large upfront deposits, unexpected fluctuations, and avoid surprise “audit traps” from salary fluctuations.

Managing the Total Human Capital

Budtender’s salaries are the engines of dispensaries, determining how quickly and smoothly a business moves. But workers’ comp is the friction factor that must be accounted for.

Dispensaries, and all cannabis brands, cannot scale on cheap labor. What you save in payroll costs will eventually catch up to you in the cost of turnover, accident payouts, and increased insurance premiums. Giving employees raises is a necessary and important piece of doing business, as long as all of the associated costs are accounted for in advance.

When you’re ready to invest more in your employees, don’t just budget for the raise—budget for the protection too. Your cannabis insurance broker can help with these calculations with a Salary Sensitivity Analysis that looks at all factors and costs of a raise, so that dispensaries can pay their employees fairly and cover all associated costs, with no surprises at the end of the year.